Updated on

August 4, 2025

US Data Center Power Demand Surpasses 150 GW, With PJM and ERCOT Accounting for 60% of the facilities

Key Takeaways:

– U.S. data center power demand has surpassed 150 GW, with tech majors shifting focus toward grid-aligned siting and long-term procurement stability.

– PJM leads with 67 GW of data center capacity, as growth accelerates in Central Virginia and Southern Pennsylvania.

– ERCOT hosts 20 GW of data center load, concentrated around major hubs such as Dallas, Houston and San Antonio.

– CAISO totals 8 GW, anchored in Silicon Valley, though development is increasingly migrating to Nevada in pursuit of scalable interconnection.

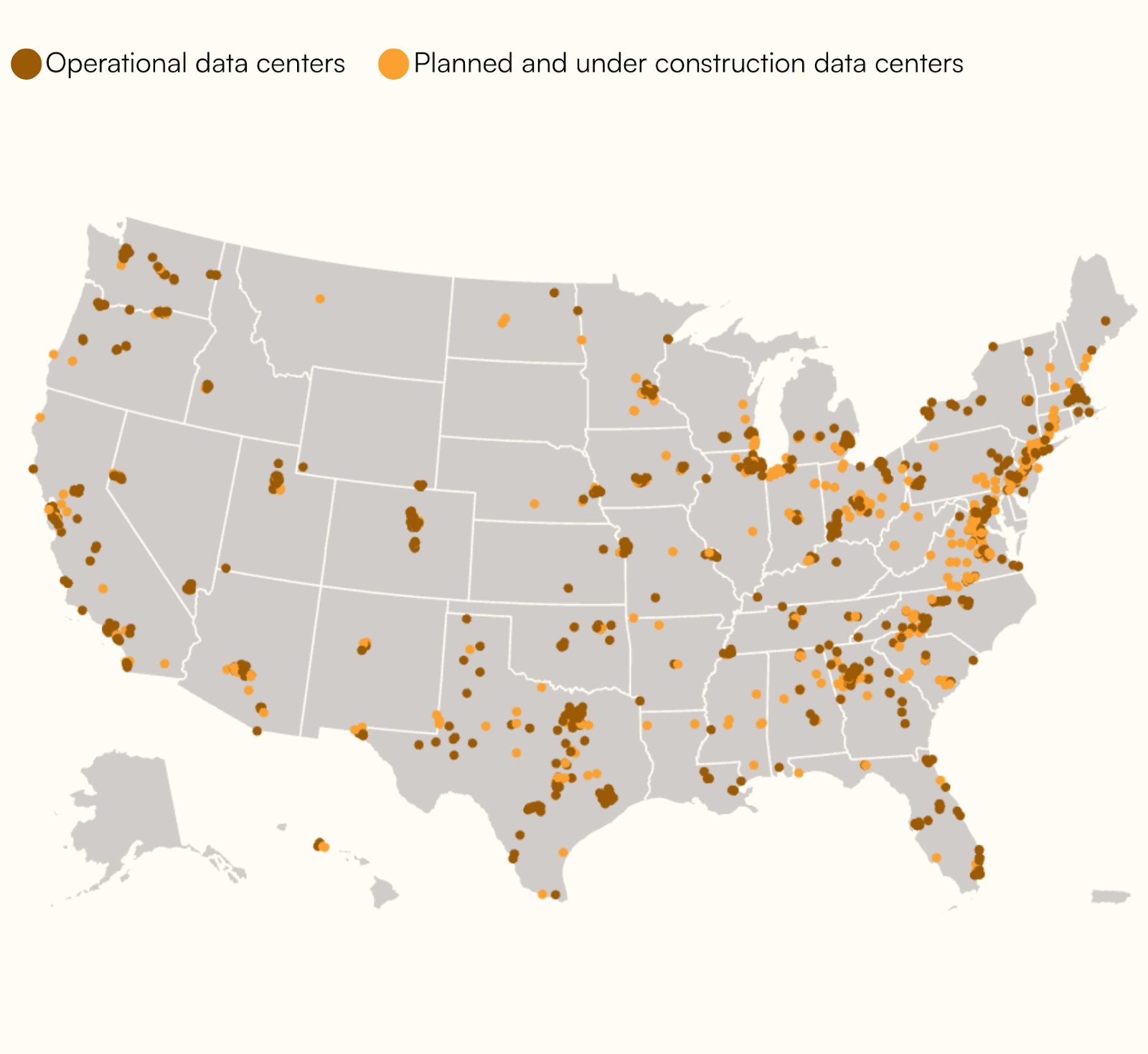

[August 4, 2025] – Enerdatics’ US Data Center Overview – August 2025 finds that cumulative power demand from operational and planned data centers across the U.S. has surpassed 150 GW, driven by a surge of new deployments in both legacy tech corridors and emerging secondary markets. As power demand scales, developers and suppliers are recalibrating around grid-aware siting strategies, navigating growing constraints in interconnection capacity, land availability, and localized price volatility.

PJM remains the largest market, accounting for more than half of nationwide development activity, supported by maturing transmission infrastructure and hyperscale load concentration. ERCOT follows, with over 20 GW of planned and operational capacity, while West Coast growth is increasingly centered in the CAISO region, where developers are responding to tightening grid conditions and shifting procurement patterns.

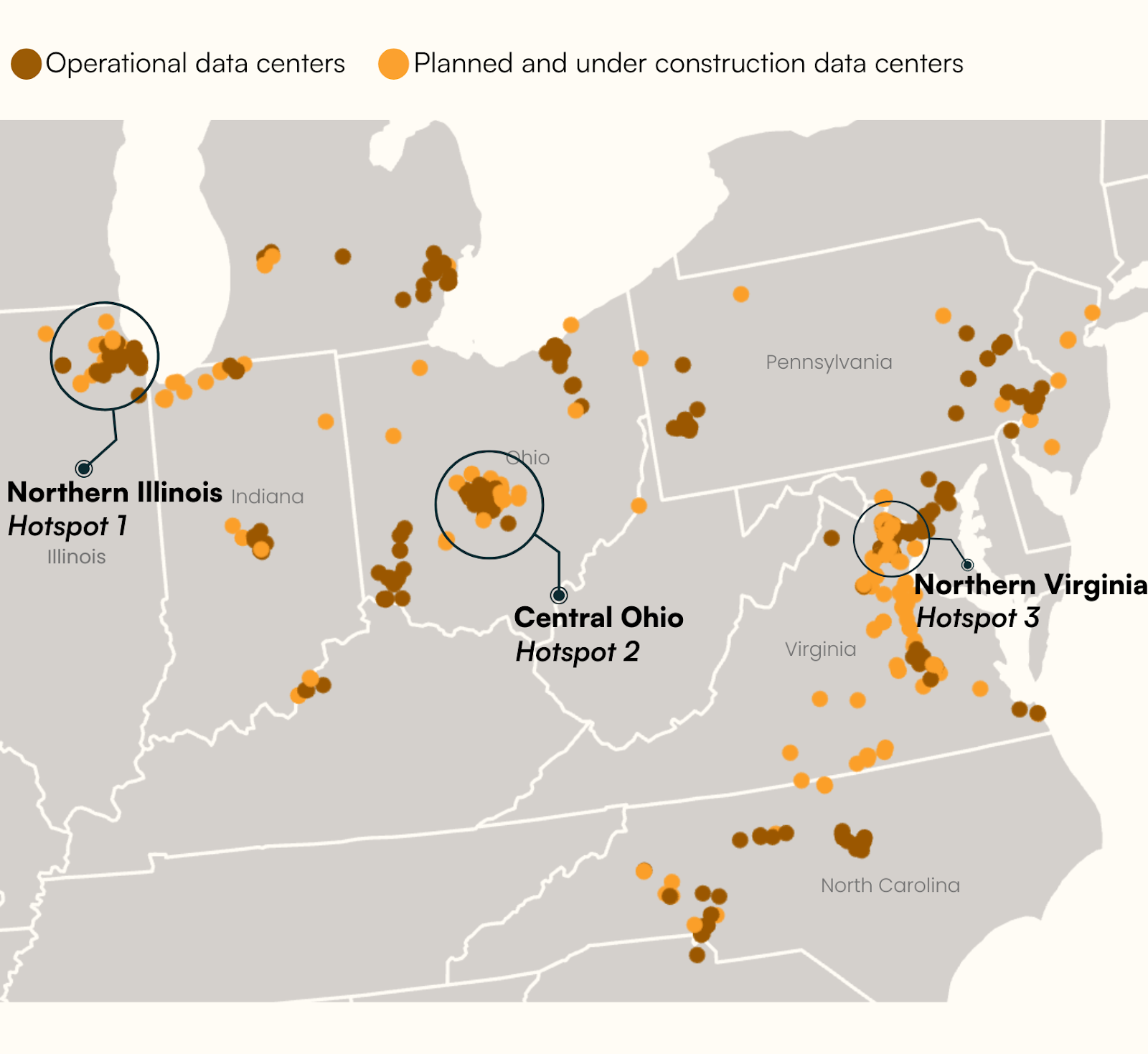

PJM Market: 67 GW of Data Center Load, with Central Virginia Leading New Development

PJM continues to lead national development, with growth intensifying in new corridors such as Central Virginia and Southern Pennsylvania. While legacy hubs remain active, developers are prioritizing areas with clearer interconnection pathways and faster approval cycles. Momentum in renewables is also converging with hyperscale demand across this region, driving interest in near-term offtake opportunities. PPA prices in PJM remain relatively stable, with Virginia and Illinois offering competitive rates in the low $30s per MWh, while Ohio continues to show wider variability based on location and congestion.

“Procurement is no longer just about location—it’s about anticipating where transmission capacity and load growth align,” said Aniket Singh, Lead Analyst at Enerdatics.

ERCOT Market: 20 GW+ of Load Anchored in Four Hubs, With Half Already Operational

In ERCOT, major metro zones like Dallas, Houston, and San Antonio continue to attract hyperscale buildout. Yet the disconnect between where data center demand is concentrated and where renewables are being deployed is prompting a strategic pivot toward virtual PPAs and flexible procurement models. Market volatility remains a key theme, reinforcing the importance of grid-aware planning. ERCOT pricing is highly location-dependent, with metro zones like Houston experiencing volatility in the $55–115/MWh range, contrasting with more stable pricing near $100/MWh in West and North Texas.

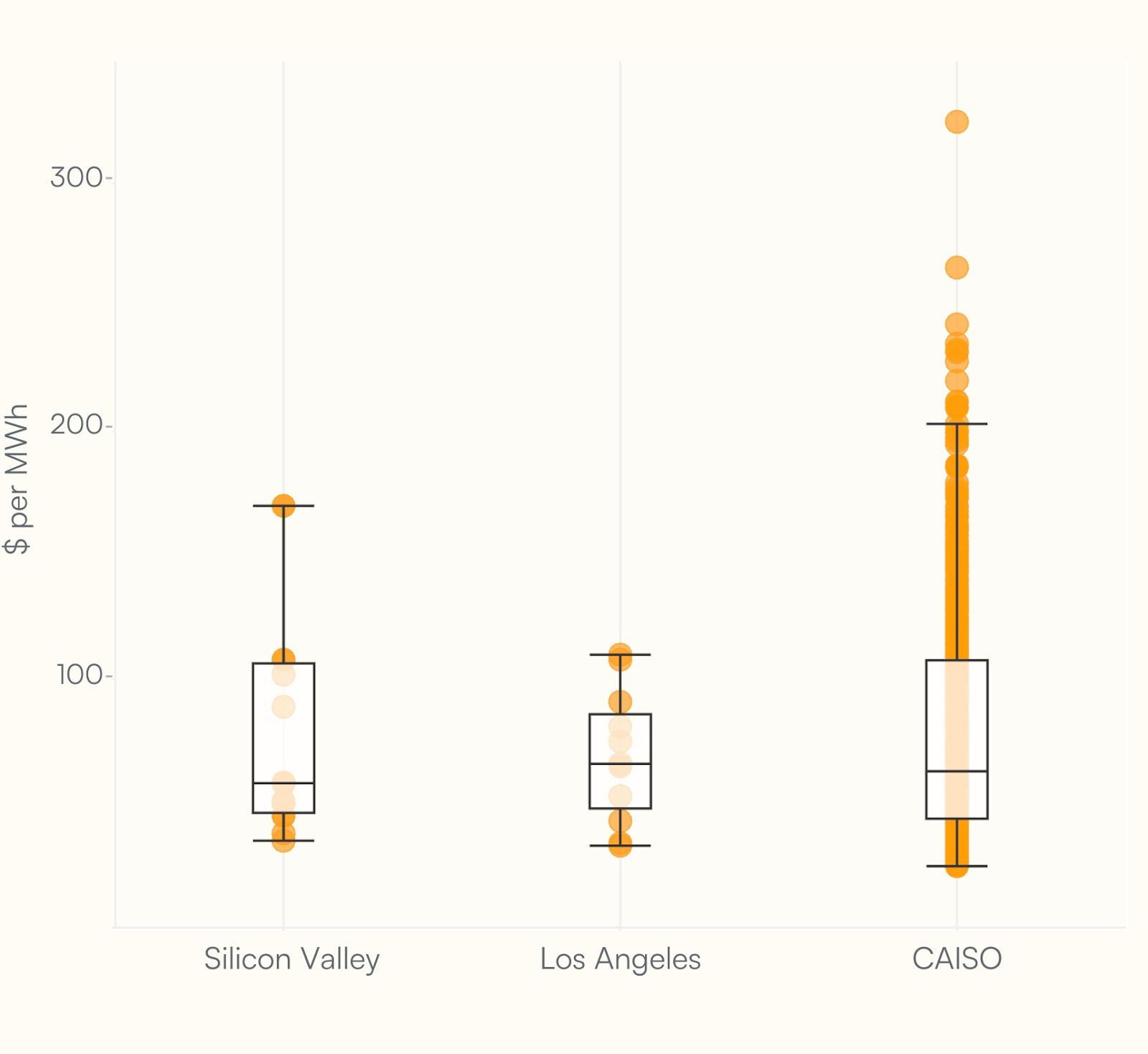

CAISO Market: 8 GW Load Centered Primarily in Silicon Valley, with Developers Shifting East to Nevada

CAISO is seeing a gradual eastward shift in development, with Nevada emerging as a preferred alternative to congested California nodes. While Silicon Valley and Los Angeles remain core demand centers, faster permitting and scalable interconnection in adjacent states are attracting both developers and corporate offtakers seeking more reliable access to low-carbon power. In CAISO, PPA prices are among the highest in the U.S., with a median around $63/MWh—utility buyers often pay over $70, while corporations are securing lower-cost deals in the $35–55 range.

About Enerdatics

Enerdatics is a business intelligence platform delivering data, insights, and analytics on renewable energy and data center industry across the globe. The company offers exhaustive datasets on M&As, Opportunities, Financings, and Power Purchase Agreements (PPAs), augmented by granular data on Projects. Founded in October 2021, Enerdatics is currently a data partner to several large-cap energy majors, among other clients.

For media inquiries, please contact:

Vini Pandit

📧 vini@enerdatics.com

📞 +1-832-699-9293

Want to explore the full Deal analysis?

Enter your business email to access deeper insights on project activity, developers, and market trends.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

.png)

.png)

.png)

.png)